Capitol Hill, washington DC 20003

Capitol Hill

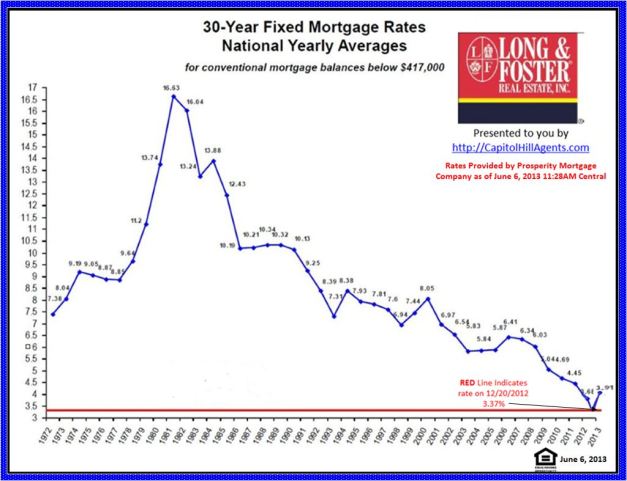

Farewell 3% mortgage rates

By Les Christie @CNNMoney June 6, 2013: 10:19 AM ET

In the past month, rates have been on the rise and they are expected to continue to climb

This week, the average rate on a 30-year fixed-rate mortgage jumped another 10 percentage points to 3.91% and are up from 3.3% in early May, according to mortgage giant Freddie Mac. Meanwhile, those seeking a 15-year loan received an average rate of 3.03%, up from 2.56% — a record low.

“It’s unlikely that rates will ever be that low again,” said Doug Duncan, Fannie Mae’s chief economist.

Those who didn’t take advantage of record-low rates have missed the boat — at least for now. Here are three reasons why.

Related: Best deals on real estate

The Fed is going to stop bolstering the housing market. The Fed has kept rates at rock-bottom levels by buying up to $85 billion a month of Treasury bonds and mortgage-backed securities. That has enabled lenders to sell mortgage loans at low interest rates and recoup their money immediately — plus profits.

“Up until recently, expectations were that the Fed would begin to taper purchases of mortgage-backed securities (MBS) and Treasury bonds late in 2013, but that timeframe appears to have moved to September, possibly sooner,” said Keith Gumbinger, vice president of HSH.com, a mortgage information company.

Related: McMansions are making a comeback

If the Fed stops purchasing the securities, private investors will have to pick up the slack. For investors to do that, the loans will have offer a better payoff. And that would mean raising rates for borrowers, said Duncan.

The economy is no longer reeling. During the recession, the Fed lowered its short-term interest rate to near zero in order to stimulate the economy. But now conditions have improved considerably since the economy emerged from recession four years ago. As the economic revival gains traction, it is creating a tailwind for interest rate increases, according to Gumbinger.

Low rates happen when the economy is in distress. But now, the market believes the economy is getting stronger, said Wendy Cutrefelli, a vice president in the Mortgage Banking Division of Bank of the West.

Read more: http://money.cnn.com/2013/06/06/real_estate/mortgage-rates/index.html

Study Shows Benefits of Social Media for Real Estate Marketing and Sales

By Brandon Cornett | Marketing June 8, 2013 | © 2013, All rights reserved

Originally Posted by Home Buying Institute

If you are reading this, you’re probably one of many real estate agents wondering if social media websites and social networking are worth your time. Should you incorporate Facebook, Twitter, LinkedIn or Pinterest into your real estate marketing plan? What can you expect to get out of it, in terms of business leads and ROI?

These are valid questions, and the answers aren’t easy to come by. In many ways, the success or failure of a social media marketing program comes down to the execution – not the tools themselves.

But a new study highlights the value of social media websites for salespeople. In short, salespeople who use these tools are more successful at selling than those who don’t. This study gives real estate agents, brokers and firms more reason to consider social media as a real estate marketing tool.

Study: Social Media as a Sales Tool

The study, featured in a recent Forbes article, was conducted by Jim Keenan, a widely cited authority in “social sales.”

I know what you’re thinking: Here’s a guy showcasing the value of the very services he provides to clients. It’s a fair point. In fact, the entire article reads like a thinly veiled puff piece with questionable data at its core (we are not told about the size of the study group, or other pertinent details that typically go along with surveys).

At the end of the day, we have to trust that Forbes did some kind of vetting of the study and its author. But I digress.

Here are the key findings:

- 78.6% of salespeople who use social media as a sales tool outperformed those who weren’t using it.

- More than 40% of the salespeople who were surveyed said they have closed between two and five deals, as a direct result of social media marketing.

- 50% of the respondents said they spent less than 10% of their selling time using these services. In other words, they’re getting a fairly good return on a modest investment of time and energy.

Of course, much depends on the manner in which these services are used. Saying that social media will improve your sales is like saying a telephone will make you salesperson of the quarter. They are only tools. It’s how you use them that counts.

Let’s shift gears and talk about real estate marketing.

A Strategy for Real Estate Agent Marketing

The above-mentioned study pertains to salespeople in a variety of industries. But it’s entirely relevant to real estate agents in particular. Realty professionals can bring social media into their real estate marketing programs in a number of ways.

One example would be to use Twitter as an information delivery system, providing valuable market updates to a select audience. Residents within the predefined area could follow the agent’s Twitter feed to receive information about home prices, sales data, foreclosure trends and the like.

Speaking of being social… You can follow the author on Twitter or connect with him on LinkedIn, for a steady stream of marketing insight.

Real estate agents can also use the networking capabilities of Facebook and LinkedIn to generate referral business from family and friends.

These are basic examples of using social media as a real estate marketing tool. Some agents are thinking outside the box to come up with more creative strategies.

How about using Pinterest as a visual relocation guide for people moving into the area? The person relocating would get an up-close look at neighborhoods, communities and other items of interest within the area. The real estate agent would get valuable exposure among prospective clients.

With social media marketing, imagination is the only limit.

Facebook and Twitter and Pinterest, Oh My

Many real estate agents suffer from “analysis paralysis” when attempting to launch a social media program. The first question, and often the biggest obstacle, is which service to use. First-timers often spread themselves too thin by signing up for every service available. The last thing you want is to spend more time managing your social media accounts than your real estate business.

Steve Strauss, author of the best-selling Small Business Bible, recommends zeroing in on one particular social media service, and then mastering it.

“Choose one,” he says. “But keep in mind that might not be your favorite or the one you’re the most comfortable with personally.”

Another common problem for real estate agents is that they don’t have anything interesting to share. The key to a successful social media marketing program is to share valuable information with an audience who can benefit from that information. The idea presented earlier with home prices and market updates is a good example.

Many homeowners these days are practically obsessed with property values in their area, especially in the wake of the housing crisis. So a real estate agent who provides news and information about local home prices should have no trouble getting people to subscribe or follow. The more valuable the information, the more attractive it becomes to the end-user.

For real estate agents, blogging and social media go hand in hand. Blogging programs like WordPress give agents an easy way to publish information online. Social networks provide an easy way to share that information. An obvious implementation would be to blog about local housing conditions, and then tweet the new blog post through Twitter, or share it through Facebook. The Home Buying Institute provides a Market Blogging service for this very reason.

Here again, imagination is the only limit.

Read more: http://www.homebuyinginstitute.com/news/social-media-real-estate-401/#ixzz2Vls8bwWs

Open Houses for CAPITOL HILL Zip Code 20003, Sunday August 19th, 2012 Presented to you by http://www.CapitolHillOpenHouses.com/

Capitol Hill Open Houses for Sunday May 6th, 2012 Washington, DC for Inside Pictures and to Print visit www.CapitolHillOpenHouses.com

From HBR’s 11 Most Popular Blog Posts of 2011

Nine Things Successful People Do Differently

by Heidi Grant Halvorson

Talent plays only a tiny role in your success; what really matters is what you do. This post has stayed on our most popular list for months.

1. Get specific. When you set yourself a goal, try to be as specific as possible. “Lose 5 pounds” is a better goal than “lose some weight,”

2. Seize the moment to act on your goals. Given how busy most of us are, and how many goals we are juggling at once, it’s not surprising that we routinely miss opportunities to act on a goal because we simply fail to notice them.

3. Know exactly how far you have left to go. Achieving any goal also requires honest and regular monitoring of your progress

4. Be a realistic optimist. When you are setting a goal, by all means engage in lots of positive thinking about how likely you are to achieve it.

5. Focus on getting better, rather than being good. Believing you have the ability to reach your goals is important, but so is believing you can get the ability.

6. Have grit. Grit is a willingness to commit to long-term goals, and to persist in the face of difficulty.

7. Build your willpower muscle. Your self-control “muscle” is just like the other muscles in your body — when it doesn’t get much exercise, it becomes weaker over time.

8. Don’t tempt fate. No matter how strong your willpower muscle becomes, it’s important to always respect the fact that it is limited, and if you overtax it you will temporarily run out of steam.

9. Focus on what you will do, not what you won’t do. Do you want to successfully lose weight, quit smoking, or put a lid on your bad temper?

Heidi Grant Halvorson, Ph.D. is a motivational psychologist, and author of the new book Succeed: How We Can Reach Our Goals (Hudson Street Press, 2011). She is also an expert blogger on motivation and leadership for Fast Company and Psychology Today. Her personal blog, The Science of Success, can be found at www.heidigranthalvorson.com. Follow her on Twitter @hghalvorson

For the Full article Click: http://blogs.hbr.org/cs/2011/02/nine_things_successful_people.html

Each year provides a clean slate and a chance to grab market share from competitors. Here are three tasks to get you started.

By Karl Stark and Bill Stewart | @karlstark | Jan 10, 2012

The New Year represents a clean slate for your business. You have the potential to completely change your financial and strategic position in 2012, taking market share and growing the value of your business. Instead of unachievable New Year’s resolutions, commit to doing these three things to prepare your business for growth in the year ahead.

1. Determine the reasonable “run-off” of your business.

What would happen if you turned off your company’s growth engine? If your salespeople stayed home and you stopped all marketing, would you continue to bring in revenue in 2012? For some businesses, sales would dry up in a matter of months as the business worked through its backlog. In other businesses, sales to existing customers might continue for years.

It’s important to understand this projected “run-off” of your business so that you can set sales and marketing goals to drive sales above this level. How much of Starbucks’ sales are driven by caffeine junkies who religiously visit their stores? A lot. In this case, it’s important to measure marketing spend against the incremental sales it would generate, rather than total sales. This would explain why most of Starbucks’ marketing dollars are used for in-store campaigns rather than through expensive TV ads.

2. “Zero-base” your market(s).

Your competitors are also starting the year with $0 in revenues, with varying levels of run-off. It’s important to understand how much of your market is “fully baked”—committed to you or competitors based on your strategic assets and other strengths—vs. market share that is in play. You’ll probably find that more market share is up for grabs than you think.

Here’s a historical example to show what we mean: Before U.S. automakers collapsed in the great recession, each year they would tout their market share and state that their goal was to increase share. We all know that they reached these market share goals largely by reducing price and increasing customer incentives—which destroyed profits. Achieving a market share of 30 percent in one year didn’t ensure a market share of 30 percent in the next, because most car buyers don’t purchase a vehicle every year. Automakers essentially enter a completely new market each year in which anyone can capture share.

What steps can you take to grab share that your competitors owned in 2011?

3. Determine the strategic investments you need to make this year to create competitive advantage that will last into 2013 and beyond.

Even if you do grow your business in 2012, you’ll face the same challenge on Jan. 1, 2013. So it’s a good idea to do some thinking now about the investments that will make your life easier into next year and beyond.

For example, what investments can you make this year to increase your market share and reduce that of your competitors? Maybe it’s making a key acquisition, investing in R&D, or increasing brand awareness. Identify these investments now so they can make an impact in future years—so you don’t have to work as hard next year.

http://www.inc.com/karl-and-bill/happy-new-year!-your-revenues-are-$0.html

Mood of the Market

By Tara-Nicholle Nelson, Tuesday, December 27, 2011.

With 2012 nearly upon us, many of us will be spending this week reviewing the events of 2011 and setting resolutions, goals or visions for what we’d like to accomplish next year.

It will come as no surprise that the most common New Year’s resolutions fall into the categories of getting organized and getting fit — physically and financially.

Financial fitness includes getting your real estate business in order. But you can’t set up your real estate plans for the year in a vacuum. They must be done in context of what’s going on in the market. Here are four predictions about what that market context will look like in the coming year:

1. Even more foreclosures

While I’d like to claim crystal-ball credit for this one, it doesn’t take heightened powers of prediction to foresee an uptick in the rate of home repossessions in 2012. Last fall’s robo-signing debacle and the ongoing legal fallout from it created a massive backlog in the foreclosure pipeline, meaning that banks are taking many months, even years, to actually foreclose on mortgages in default.

Earlier this year, the New York Times reported that the additional hurdles New York state courts are requiring banks to leap in the wake of the robo-signing revelations, like additional settlement meetings with the homeowner to see if a modification can be brokered, have created a backlog of foreclosures that it would take 62 years to clear, at the current rate of foreclosure.

It’s pretty clear that in 2012 and beyond, the banks will work through those backlogs. The inevitable result will be an increase in foreclosures.

2. REOs and short sales will become the new normal

If you even know anyone who has house-hunted in the past couple of years, you’ve likely heard tales of the high-drama high jinks — super-long escrows, first-time buyers being bested by investors’ cash offers, banks resistant to negotiating for repairs — that take place in the course of a distressed property sale.

In the coming year, distressed home sales will continue to represent an increasing share of homes on the market. So, buyers will shift from considering whether to buy a short sale to understanding that they must be educated and prepared to do a deal with a seller, a bank (to buy an REO) or a hybrid of the two (to buy a short sale) to access the full selection of homes on the market.

This, in turn, will empower buyers to make smart decisions about what to offer and what to expect on any listing they like, as well as to set smart priorities and make realistic comparisons between listings based on their own personal priorities around timing, certainty and seller flexibility.

3. So-called ‘smart cities’ will do well

This year, a number of housing markets saw double- or even triple-dips in home values. In others, pricing stayed relatively flat. However, in areas where technology powers the economy, home values prospered along with the industry. Silicon Valley real estate, for instance, saw fierce competition among buyers as the young employees of companies that went public like used their newly stocked bank accounts to buy their first homes.

I recently talked with Jed Kolko, chief economist for real estate search site Trulia, and his 2012 forecast was that so-called “smart cities” will continue to have hot real estate markets next year. But Kolko defined smart cities much more broadly than the California tech hubs. Other tech centers like Austin, Texas, and the Massachusetts suburbs of Cambridge, Newton and Framingham all made Kolko’s list, as did Rochester, N.Y. (a town known for its highly educated, highly skilled work force).

4. Consumers will get ‘hopeless’

I mean hopeless in the best of all possible ways. For years, buyers and sellers have been waiting for that singular event to occur that would cause a quick market recovery. But 2012 will mark the fifth or sixth year of the real estate recession, depending on who you talk to. I predict that those consumers who have not already done so will drop unrealistic hopes for a fast return to the heady real estate fortunes of the subprime era. Instead, people will make their real estate plans based on:

- today’s low home prices, rather than the fantasy of what could happen if the market miraculously came back;

- assumptions of very low, or no, appreciation in home values for years to come; and

- very conservative estimates of their own finances and how they will grow.

As a result, buyers won’t break their necks to hurry and buy before prices uptick; rather, they’ll save and plan to buy when it makes the most sense for their finances. Homeowners will do the same; they will either refi, remodel and be content where they are for the long haul, or decide their homes no longer fit their lifestyles and their finances, divest of them and move on. But the good news is, people will make these decisions based on what is or is not sustainable for their lives and their finances, and not based on inflated hopes about what the market will or will not do.

Tara-Nicholle Nelson is author of “The Savvy Woman’s Homebuying Handbook” and “Trillion Dollar Women: Use Your Power to Make Buying and Remodeling Decisions.” Tara is also the Consumer Ambassador and Educator for real estate listings search site Trulia.com. Ask her a real estate question online or visit her website, www.rethinkrealestate.com.

What Is It?

What if you want to invest in the real estate sector, but you either already have a house or don’t have enough money to buy one right now? The answer is REITs. REITs sell like stocks on the major exchanges and invest in real estate directly through properties or mortgages. A major advantage to REITs is that they receive special tax considerations. Furthermore, they typically offer investors high yields as well as a highly liquid method of investing in real estate.

What if you want to invest in the real estate sector, but you either already have a house or don’t have enough money to buy one right now? The answer is REITs. REITs sell like stocks on the major exchanges and invest in real estate directly through properties or mortgages. A major advantage to REITs is that they receive special tax considerations. Furthermore, they typically offer investors high yields as well as a highly liquid method of investing in real estate.

There is a wide variety of REITs, but you can break it down into three main categories:Equity REITs – Equity REITs invest in and own properties (thus responsible for the equity or value of their real estateassets). Their revenues come principally from their properties’ rents.Mortgage REITs – Mortgage REITs deal in investment and ownership of property mortgages. These REITs loan money for mortgages to owners of real estate, or invest in (purchase) existing mortgages or mortgage-backed securities. Their revenues are generated primarily by the interest they earn on the mortgage loans.

Hybrid REITs – Hybrid REITs combine the investmentstrategies of equity REITs and mortgage REITs by investing in both properties and mortgages.There are over 300 publicly-traded REITs operating in the United States whose average daily trading volume has more than quadrupled during the last three years, reaching over $280 million dollars. The average dividend yield of an REIT is 9-12%.

Hybrid REITs – Hybrid REITs combine the investmentstrategies of equity REITs and mortgage REITs by investing in both properties and mortgages.There are over 300 publicly-traded REITs operating in the United States whose average daily trading volume has more than quadrupled during the last three years, reaching over $280 million dollars. The average dividend yield of an REIT is 9-12%.

Objectives and Risks

REITs can be used to meet a wide range of objectives within the real estate sector. They allow you to focus on different sectors of real estate, such as residential versus commercial. They allow you to target different geographical areas. And REITs have often been thought to closely follow the performance of small- to medium-cap stocks.

Still, no matter what the market does, the performance of a REIT is determined by the value of its real estate assets. This is one major advantage to a REIT – its performance is not correlated to other financial assets such as stocks and bonds. As a result, REITs are usually less volatile and provide some degree of inflation protection.

How To Buy or Sell It

As we mentioned earlier, REITs sell like stocks on the major exchanges. Therefore, they can usually be bought through a brokerage, either full service or discount. Commissions to buy REITs are usually the same as common stock fees. There is no minimum investment for most REITs, although you may need to buy the shares in even blocks of 10 or 100. Also, many brokerages require clients to have at least $500 to open an account and trade stocks or REITs.

Strengths

|

Weaknesses

|

Three Main Uses

|

Read more: http://www.investopedia.com/university/20_investments/17.asp#ixzz1hgVdTE7b